News Event

News Event

From Trading Economics: The US government posted a USD 107 billion budget gap in August 2016, a 67 percent rise from a USD 64 billion deficit in the same month a year earlier and in line with market expectations of a USD 108 billion gap. Outlays rose 23 percent to USD 338 billion while receipts increased at a slower 9.5 percent to USD 231 billion. Government Budget Value in the United States averaged -16361.75 USD Million from 1954 until 2016, reaching an all time high of 189796 USD Million in April of 2001 and a record low of -231677 USD Million in February of 2012. Government Budget Value in the United States is reported by the Financial Management Service, US Treasury.

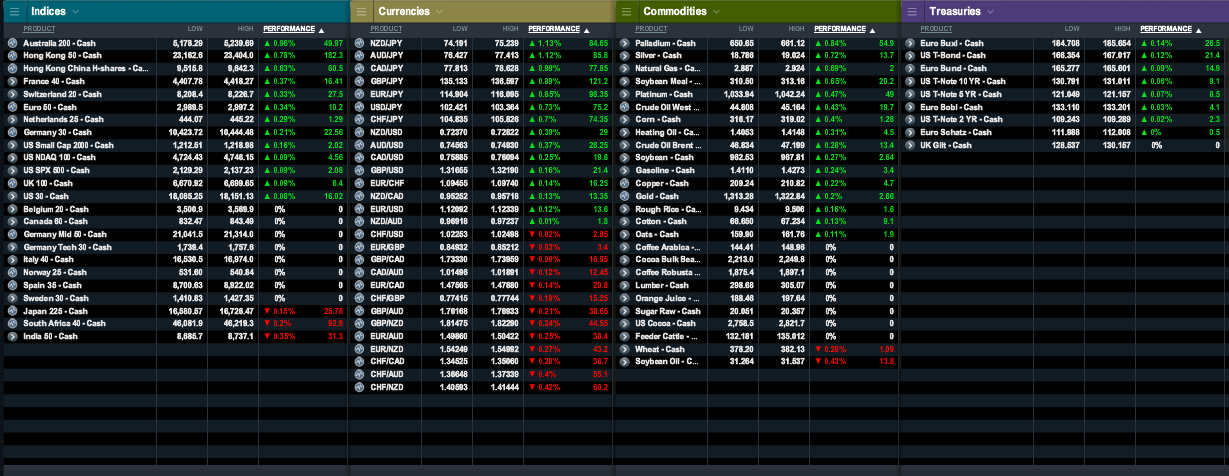

Market Snap

Overview of Currencies

USD:

Overview of Currencies

USD: The Federal Reserve are most likely to leave their current policy unchanged at their next meeting as inflation data has yet to show the necessary improvement needed to warrant additional hikes. If the bank did change its policy in the next 3 months then the move would most likely be a rate hike, especially considering recent Fed rhetoric with many members stating that the US economy is moving closer towards the Fed's objectives. This gives the USD currency an overall bullish tone for the next 3 months.

EUR: The ECB are most likely to leave their policy unchanged at their next meeting because they have already cut their main rates heavily over recent years and they are at what many experts consider to be an ultimate low. If the bank did conduct a policy change within the next 3 months then the most likely move is an increase in its QE programme, because it is still battling low inflation alongside low interest rates, so more powerful action could be needed. This gives the EUR currency an overall dovish bias over the next 3 months.

GBP: The BoE have now officially entered an easing cycle by announcing on August 4 a 25 basis point cut to the Bank Rate and a surprise 60 billion increase in their Asset Purchases. Along with the surprise increase in QE the BoE also stated "the majority of the MPC expect rates to be near 0% by the end of the year" which would imply that another rate cut of 25 basis points can be expected before the year end. Given the BoE's latest monetary policy decisions and expectations for further easing this year, we maintain a bearish bias for GBP.

AUD: There is a strong possibility that the RBA will ease policy again during 2016 as many economist believe the door for further easing remains open due to continued low inflation in Australia. As such inflation data for Q3 will be key in regards to future policy expectations, Q3 CPI is not released until October and therefore although the RBA will likely leave policy unchanged at their September meeting, further easing in later meetings remains a strong possibility especially if Q3 CPI disappoints. This therefore maintains our bearish bias for AUD.

NZD: Although inflation in New Zealand could continue to warrant further cuts by the RBNZ, recent rhetoric has downplayed the need for further easing and therefore reduces the likely of any change in monetary policy in the near future. If the RBNZ was to change policy in the next 3 months then the move would likely be a further 25 basis point cut with a miss in Q3 inflation as the most likely cause. We therefore hold a weakly bearish bias for NZD.

CAD: The BoC are most likely to leave monetary policy unchanged at their next meeting as Canadian inflation is within the BoC’s target range of 1-3% with the economy also supported by accommodative fiscal measures. If the BoC did conduct a policy change within the next 3 months it would likely be a rate cut based on concerns over Canada’s competitiveness since CAD’s appreciation throughout the year. Although this gives CAD a slightly bearish fundamental bias, with most central banks currently in easing cycles CAD has a comparatively neutral bias.

JPY: The BoJ will most likely need to ease policy further in the near future as the increases made to its ETF purchases and USD lending programmes will likely be insufficient in helping inflation reach its target of 2%. Furthermore Kuroda’s pledge to "conduct a comprehensive assessment" of economic and price developments when the BoJ next meet highlights that further easing is still on the table. With further easing by the BoJ likely we continue to maintain a fundamentally bearish view on JPY, however due to its status as a safe haven currency JPY will likely strengthen in times of risk off sentiment.

CHF: The SNB are most likely to leave their policy unchanged at their next meeting as interest rates in Switzerland already remain at a record low of -0.75%. If the SNB were to change policy in the next 3 months it would likely be a rate cut as inflation continues to remain far below the SNB’s target. This gives CHF an overall bearish tone.

Source: Jarratt Davis